|

|

|

|

|

| Author |

|

|

Did you get the memo?

Join Date: Mar 2003

Location: Wichita, KS

Posts: 33,007

|

Quote:

__________________

07 Mazda RX8 Past: 911T, 911SC, Carrera, 951s, 955, 996s, 987s, 986s, 997s, BMW 5x, C36, C63, XJR, S8, Maserati Coupe, GT500, etc |

||

03-09-2009, 09:58 AM

03-09-2009, 09:58 AM

|

|

|

Registered

Join Date: Dec 2002

Location: Delaplane, virginia

Posts: 491

|

Rick Lee-

Things might not be as bad here as you think...the market here is better than the rest of the Country right now. Commercial leasing is rising...the Stimulus Bill and all people planning on feeding off it are moving into town...So you could probably re-rent it quickly.

__________________

01 996TT 2003 M5 1979 930 (sold) BMW 1200 GS Adv&BMW 100/7 F350 Diesel |

||

|

03-09-2009, 10:06 AM

|

|

|

Registered

Join Date: Oct 2006

Location: Colorado, USA

Posts: 8,279

|

Quote:

Putting money down is highly relevant. In any given situation, someone who put down 20 or 30% is far more likely to not walk away from that. He has a sizeable cash investment that he would be tossing away, immediately, when he walks. He has to analyze whether that is worth it, or whether he should stay in the house and try to wait for it to rise in value again, so he doesn't realize his loss. But when the homeowner put no money down, and has no skin in the game, it makes it much easier to walk. Last edited by the; 03-09-2009 at 10:09 AM.. |

||

|

03-09-2009, 10:07 AM

|

|

|

Did you get the memo?

Join Date: Mar 2003

Location: Wichita, KS

Posts: 33,007

|

Quote:

Obviously walking on $138k or $92k would be painful, but I'm sure you could still justify walking with a "good money after bad" argument. It's easy to blast the banks for not assessing a property's "true" value, but you would have needed a psychic for that. Remember that we all have the benefit of hindsight, I don't think most saw the bottom dropping out of the market this quickly or to this degree.

__________________

07 Mazda RX8 Past: 911T, 911SC, Carrera, 951s, 955, 996s, 987s, 986s, 997s, BMW 5x, C36, C63, XJR, S8, Maserati Coupe, GT500, etc |

||

|

03-09-2009, 10:44 AM

|

|

|

Registered

Join Date: Jul 2004

Location: Maryland

Posts: 31,753

|

There are a thousand permutations in a contract, in life. How you deal with them gets to the heart of the person.

When I sign a contract, I uphold my end. I nearly lost my farm the year after I bought it because the person I entered into a rent to buy contract (done by my lawyer and signed by all parties) on another property I owned, walked. I then got orders out of state (unexpected, needs of the Navy) and had to eat the commute and lodging. My wife and I did all the right things, sold the '83 SC, scrimped and made it through. But walk of my own volition? It is not in me, or anyone I'd want to know. You guys can dress the pig in untold guises, I'm not paying for the dry cleaning.

__________________

1996 FJ80. |

||

|

03-09-2009, 11:09 AM

|

|

|

Banned

Join Date: Sep 2006

Location: South of Heaven

Posts: 21,159

|

Quote:

|

||

|

03-09-2009, 11:12 AM

|

|

|

|

Registered

Join Date: Jun 2005

Location: Hamburg & Vancouver

Posts: 7,693

|

Quote:

But each person is differentas are the circumstances of each contract and the manner in which that contract was negotiated and agreed. A lifetime in the law has taught me that law and justice are two different things and that the law is frequently an ass. I can certainly visualize scenarios where walking away from some serious negative equity is a choice I would make. I certainly wouldn't do that lightlybut I can imagine such a scenario nevertheless. My field was corporate finance and I spent many years working with banks all over the world. Strangely (or perhaps not) I have very little respect or sympathy for the banking profession today. When it came down to the short strokes I have never, ever seen a bank make a decision by reference to moral principles. Never.

__________________

_____________________ These are my principles. If you don't like them, I have others.Groucho Marx |

||

|

03-09-2009, 11:57 AM

|

|

|

Registered

Join Date: Oct 2006

Location: Colorado, USA

Posts: 8,279

|

Quote:

Many of us saw this coming, it was no surprise at all, and banks lending out billions of dollars should have seen it, too. It wasn't hard at all to see. There were so many things that made it easy. Just a few: (1) It happened before. (2) You can't have an asset like real estate, which pokes along at a relatively stable, slow appreciation rate, suddenly double or triple in value in a few years, and expect that to hold. As was said in the More Bad RE News thread, over and over again in real time through 2006 and 2007, only a total idiot/clueless/naive person could think that. Last edited by the; 03-09-2009 at 12:33 PM.. |

||

|

03-09-2009, 12:30 PM

|

|

|

Did you get the memo?

Join Date: Mar 2003

Location: Wichita, KS

Posts: 33,007

|

Quote:

It's one thing to say, "this can't continue". It's quite another to determine a precise property value based not on what it is selling for today, but what it will be worth in an undetermined future recessionary period. By the way, how does this have anything to do with skipping out on a commitment? What I don't understand is the fact that when the home was purchased, it was obviously worth X dollars. Unless it was bought to flip, why is it suddenly no longer worth X dollars to the homeowner? Simply because houses are now selling for less?

__________________

07 Mazda RX8 Past: 911T, 911SC, Carrera, 951s, 955, 996s, 987s, 986s, 997s, BMW 5x, C36, C63, XJR, S8, Maserati Coupe, GT500, etc |

||

|

03-09-2009, 01:06 PM

|

|

|

?

Join Date: Apr 2002

Posts: 30,897

|

Quote:

? ?

|

||

|

03-09-2009, 01:18 PM

|

|

|

Registered

Join Date: Jul 2004

Location: Maryland

Posts: 31,753

|

Quote:

I share all of your life lessons and some lack of respect for the banking profession today. And the law is indeed frequently an ass. My sister is a DA and I'll pass along our respects  All that said, the nuance of contracts law and the simple terms of a mortgage are completely different animals. Beyond the diligence necessary to make sure the house you are buying is as advertised and meets code, there is little to a mortgage contract terms that requires more than rudimentary math. My favorite professor at Cal had a term, "ditch digging": Read the terms, do the math, dig the ditch. His point was that most transactions, most contracts always start with a estimate on how much the ditch was going to cost and then they work from there. Focus on the ditch first, the basics. Here is the rub I have with the OP: he, like many others, were gambling, were willing participants in financial schemes they hoped was mortgage upsidasium...and they thought that they would win. I simply cannot, if he can afford to stay and live where he is, brook any bravo sierra from him, anymore than a Casino in Vegas would if he had lost at cards. Bankruptcy laws never intended to put a safety net under his sorry ass. I have owned a number of businesses and have engaged in a lot of contracts: The only time I walk is to chase and punish the SOBs after they didn't own up to their part of the bargain, didn't dig the ditch. I have only lost once. My fault. Sorry for the ramble.

__________________

1996 FJ80. |

||

|

03-09-2009, 01:19 PM

|

|

|

Bandwidth AbUser

Join Date: Nov 2001

Location: SoCal

Posts: 29,522

|

How does the IRS treat this jingle mail? It seems that a loss eaten by the bank when the homeowner mails in his keys is a gain for the defaulter.

__________________

Jim R. |

||

|

03-09-2009, 01:36 PM

|

|

|

|

Registered

Join Date: Oct 2005

Location: Magnolia State

Posts: 7,548

|

Paul, while I certainly understand your point (and share your morality sentiments), would you not agree that some of our most "successful" entrepreneurs routinely walk away from sour business deals rather than honoring their original commitment? Many of these folks use bankruptcy and default as nothing more than a business tool. Trump comes to mind.

That being said, more than one of successful business people I personally know have gone broke, lost fortunes but always seem to land on their feet and come back even wealthier.

__________________

Jim 1987 Carrera 2002 BMW 525ti 1997 Buell Cyclone cafe project 1998 Buell S1W: "Angriest motorcycle I've ever ridden." |

||

|

03-09-2009, 01:43 PM

|

|

|

Registered

|

Quote:

__________________

2022 BMW 530i 2021 MB GLA250 2020 BMW R1250GS |

||

|

03-09-2009, 01:48 PM

|

|

|

Registered

Join Date: Oct 2006

Location: Colorado, USA

Posts: 8,279

|

Quote:

It was called in 2006 that RE in the bubble areas would go down in value at least 50%. Charts were posted, showing almost exactly how much this would fall (it is reverting to the mean, i.e., correcting back to where real estate appreciation tracks the general rate of inflation), and when it would fall. They turned out to be almost exactly correct. Also, you don't need to know the value for any real estate. Only the bubble areas. The other stuff doesn't matter much. I read yesterday that this whole crisis was caused by the bubble in only 40 counties throughout the US - those bubbly ones we all talked about in 2006-07. If the banks would have seen that information, and opened their eyes, all of this would have been averted. It really didn't take a genius to figure it out. What the banks did was a massive failure, based mostly on short term greed, which clouds judgment. Last edited by the; 03-09-2009 at 01:57 PM.. |

||

|

03-09-2009, 01:52 PM

|

|

|

Bandwidth AbUser

Join Date: Nov 2001

Location: SoCal

Posts: 29,522

|

Quote:

http://www.irs.gov/individuals/article/0,,id=179414,00.html also this... http://www.irs.gov/pub/irs-pdf/p4681.pdf If I'm reading the irs docs correctly, abandonments (what the OP is talking about doing) have tax different treatment than simply being foreclosed on.

__________________

Jim R. Last edited by Jim Richards; 03-09-2009 at 02:03 PM.. |

||

|

03-09-2009, 01:54 PM

|

|

|

Registered

|

I have no info on anyone's individual situation. But I wanted to remind us all that, in the long-ago days of 2004-2005, in California, 90% of everything the average person heard, read and saw was telling them if they didn't buy at the prices then, they would never be able to own a home. They would be a permanent renter, a lifelong loser, forever shut out from the American Dream. Lots of apparently authoritative people said this, the media and all manner of books said this. Meanwhile prices were steadily moving out of reach.

There was tremendous pressure to stretch and buy a house, while one still could. Yes, some of those people were gamblers, schemers, and speculators. But others were simply ordinary people (who didn't read the "More Bad RE News" thread closely enough) who were trying to do what they thought they had to do. They were wrong, and they will lose a lot of money, but I wouldn't necessarily tar them with the "gambler" brush. Quote:

__________________

1989 3.2 Carrera coupe; 1988 Westy Vanagon, Zetec; 1986 E28 M30; 1994 W124; 2004 S211 What? Uh . . . he and him? |

||

|

03-09-2009, 02:42 PM

|

|

|

Registered

Join Date: Oct 2006

Location: Colorado, USA

Posts: 8,279

|

Quote:

|

||

|

03-09-2009, 02:49 PM

|

|

|

Registered

Join Date: Oct 2006

Location: Colorado, USA

Posts: 8,279

|

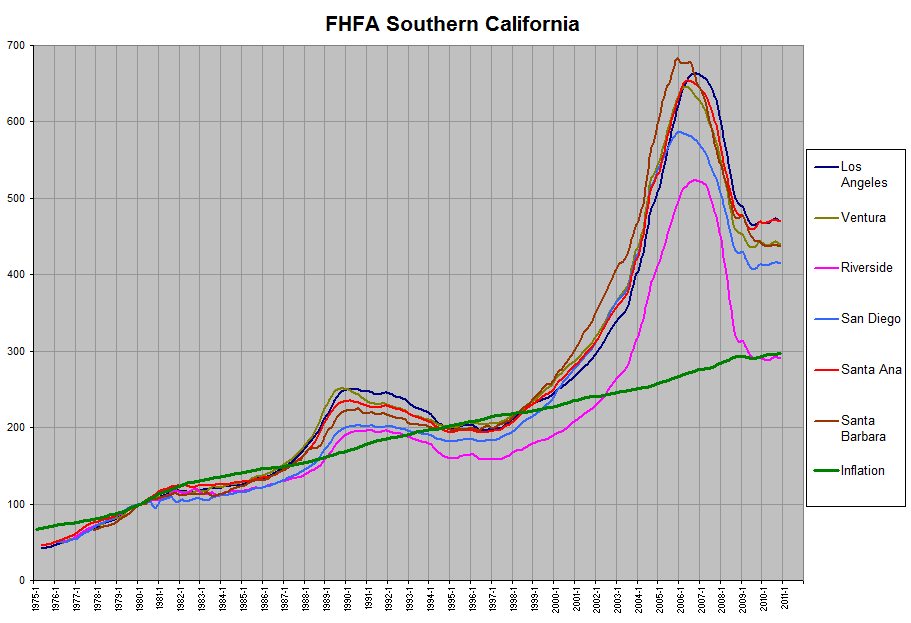

How anyone could have thought, in 2006 (and earlier) when this graph was posted, that the practically straight up appreciation line could EVER be sustained, is nuts. Anyone who has lived at all for a few decades and paid even loose attention to real estate could see what was going to happen.

Like many said in 06, it's a simple bell curve, which will revert to the mean (i.e., the green inflation line). Anyone with an ounce of common sense could see that. It was expressly called in 2006, and the chart has followed precisely as planned. There is no other way it could go. What goes up like that bubble MUST come down the other side, simple bell chart. Anyone who looked at this chart in 2005/06 and didn't agree there was a major bubble was, simply put, extremely ignorant.

|

||

|

03-09-2009, 02:56 PM

|

|

|

Registered

Join Date: Jul 2004

Location: Maryland

Posts: 31,753

|

Quote:

It is quite unfortunate, in my mind, that the ethos of the art of the deal has sunk into the most basic contract, a house...a house has never been an investment leader, rather a small part of the portfolio. That a house got elevated in the investment matrix speaks volumes about financial amateurs. Again, dig the ditch first, based on time honored investment principles. Believe me, I am no Pollyanna in finance and business...but I think we are into Apples and Oranges where the OP was headed. Dueller, you and I can seek advantage on each other in a business deal, but if either of us defaults, at least in my world, that is a death knell for the loser in terms of future relationships. Reputation should matter, it does to me. Not arguing...you are another poster I respect.

__________________

1996 FJ80. |

||

|

03-09-2009, 02:58 PM

|

|

Only Porsche

Only Porsche Only bike

Only bike 1989 Porsche 911 Carrera 3.2

1989 Porsche 911 Carrera 3.2